(© Feng Yu - stock.adobe.com)

NEW YORK — Many Americans have a love-hate relationship with their credit cards — and for half, their credit cards are their lifesavers. A survey of 2,000 people with poor, unknown, or no credit finds that most Americans struggled with managing their finances when they first moved out on their own (56%).

Nearly three in five say that one of the toughest parts of becoming an adult was learning about how credit works (58%).

Results also show that two in five people (41%) don’t think there are enough resources available to them to help learn about credit. More than half the poll (58%) wishes they had a handbook they could reference to help answer questions about credit.

What is credit anyway?

Conducted by OnePoll on behalf of Oportun, the survey finds people are most likely to get information about credit from the internet (52%) or banks (37%). Although 35 percent prefer to get their information straight from the source — credit card companies — most people think the companies overcomplicate credit by using jargon or fine-print limitations (59%).

Despite the average person having two credit cards open right now, nearly a quarter of Americans (24%) think that credit card companies don’t make it easy to open a new card. The most common reasons credit card companies deny people from getting a credit card include not having enough credit history (35%), having too much debt (35%), and not having enough income (34%).

“We estimate there are 100 million people in the U.S. who are effectively locked out of the financial mainstream because they either don’t have a credit score or have been mis-scored by the major bureaus. For many people this is a maddening Catch-22: how do I build credit when no one will loan me money to build credit with?” says Matt Jenkins, COO and GM of Personal Loans at Oportun, in a statement. “The good news is that some lenders now use technology and alternative data to make responsible credit available to people without a score.”

Monthly credit card payment peril

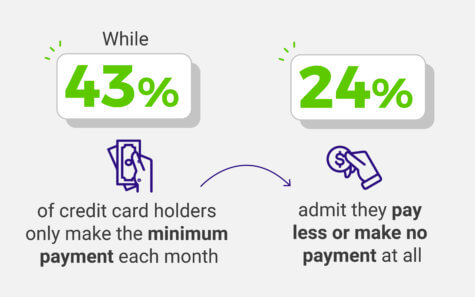

Aside from trying to open credit cards frequently, the poll finds that there may be other habits at play that are affecting Americans’ credit scores. Those with credit cards have taken an average of two cash advances, which is likely to pull their score down a bit. One in five don’t make payments to their credit card every month (21%) and 43 percent only opt to pay the minimum amount due.

Aside from trying to open credit cards frequently, the poll finds that there may be other habits at play that are affecting Americans’ credit scores. Those with credit cards have taken an average of two cash advances, which is likely to pull their score down a bit. One in five don’t make payments to their credit card every month (21%) and 43 percent only opt to pay the minimum amount due.

Surprisingly, nearly a quarter of those with credit cards admit they pay less than the minimum amount due or make no payment at all (24%). Many don’t realize that when you pay matters, too; respondents with credit cards have made an average of two late payments within the last year.

More than two in five have difficulty keeping track of the credit cards that they own (44%) and a similar amount admit that they’re so deep in debt that they don’t even know where to begin to pay it off (41%). Despite 54 percent feeling confident in understanding how to build good credit, the survey finds Americans still fall for credit myths all the time.

The myth about ‘good’ credit

Half of Americans incorrectly identified credit scores under 670 as being “good credit.” Nearly one in four still think checking their credit report will lower their credit score (24%) and another 18 percent believe closing a credit card will increase their credit score when the exact opposite is true.

Half of Americans incorrectly identified credit scores under 670 as being “good credit.” Nearly one in four still think checking their credit report will lower their credit score (24%) and another 18 percent believe closing a credit card will increase their credit score when the exact opposite is true.

One in five believe that as long as their debt is paid off, their negative history including late or missed payments will be erased (21%). The same amount also incorrectly believe that credit scores are the only thing that lenders consider.

“A credit score impacts more than how much you pay in interest, it can also determine the kinds of employment you can hold, where you can live, and more,” Jenkins explains.

“Consumers who find themselves with no or low credit should seek responsible lenders, those with APRs below 36 percent who will report their payments to the credit bureaus. By making their payments on-time and in-full, consumers can quickly start to build the good credit scores they deserve and that will open new pathways to better financial outcomes.”

Only pay the new balance, anything you have charged since then is an interest free loan carried to the next billing cycle (assuming your waived all interest if paying the new balance in full).

Important note: The interest waiver only apples if the ENTIRE new balance is paid. Miss by a penny, you pay interest on ALL charges from the date charged.

(Check terms and conditions of CC agreement)