(© Christin Lola - stock.adobe.com)

NEW YORK — The “five-year plan” is dead, as the average American is now planning 12 years ahead as they rethink their futures. A survey of 2,000 working Americans finds that when thinking about saving money for retirement, a five-year plan simply isn’t going to cut it.

Nearly three-quarters of respondents said the five-year plan is less achievable today than ever before (74%) because of rising household expenses (59%), inflation (49%), and school debt (43%). Interestingly, Gen Zers (53%) are just as worried as baby boomers (54%) about whether or not they’ll receive Social Security benefits, citing that this makes the five-year plan less achievable to them.

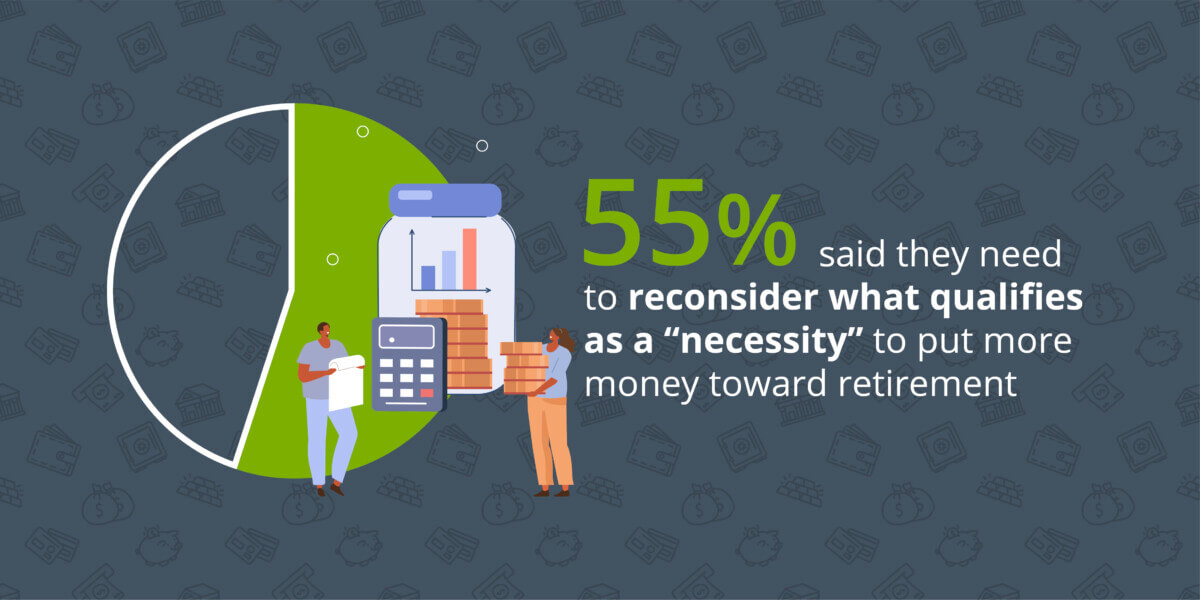

Conducted by OnePoll for SurePayroll for National 401(k) Day, the survey also found that when thinking about their financial future, 55 percent of Americans said they need to reconsider what qualifies as a “necessity” to put more money toward retirement. To get a head start on saving money for the future, 57 percent are already saving for retirement. To help reach their goals, nearly four in 10 would take a second job to help put money towards their future (39%). Others would prioritize necessary purchases and cut down on impulse spending (48%), while another 46 percent would work extra hours at their job.

“Employers helping employees achieve their financial goals is good for small business growth, good for employee retention and good for the community,” says Gabriela Rodriguez, 401(k) product marketing manager at SurePayroll, in a statement. “Offering employees a retirement plan also helps relieve stress for their future, which is especially important for Generation Alpha.”

Retirement is getting farther and farther away

A quarter of employed Americans admit that despite their efforts, they’re not close to achieving their retirement goals today — especially millennials (22%) — leaving 59 percent of all respondents wishing that they started saving sooner. Consequently, one in eight also don’t currently feel prepared for retirement.

While most respondents whose employer offers a 401(k) are enrolled in it (71%), one in five aren’t (19%). Employed Americans who work at a small business are more likely to enroll in their employer’s 401(k) option (82%) than those who work at a private company (72%) or public company (61%). Those who do participate in the plan said that their employer’s contribution adds value (57%), doubles the value when they do match (56%), and has helpful tax benefits (49%).

Working adults are also being proactive outside of the workplace; 57 percent have a separate retirement fund from what their employer offers, including a majority of those who utilize that offer (74%). Half of the respondents who have not started saving for retirement yet said they’re waiting for their employer to offer or explain more about a retirement plan, and 43 percent said they haven’t had the time to start.

Millennials’ top reasons for not saving for the future yet are also waiting for their employer to offer more information (60%) and not knowing where to start (40%). Those whose employer does offer a 401(k) plan but don’t participate in it said they just need all their income for other expenses now (61%) and that their employer simply doesn’t contribute enough to make this option feel worthwhile (43%). Onboarding is the most popular time to sign up (42%) and the majority (57%) of Americans who are enrolled in a 401(k) plan based their decision on employer-provided materials.

“Employers play an important role educating employees on the value of their retirement benefits,” Rodriguez says. “They should emphasize the value of their 401(k) plan—each dollar contributed during your 20s can grow to $17 by the time you retire—and promote sign up instructions during onboarding and throughout the year.”

It’s all about the benefits

Whether or not they use them, benefits like retirement planning matter in how people think about their employer. After health care (49%), a 401(k) plan with a match (47%) was the top non-cash benefit that would impact their choice of whether or not to stay with their employer. This was followed by a 401(k) without a match (32%) and mental health benefits (29%).

Respondents who work at small businesses are especially partial to a 401(k) with an employer match (50%) as opposed to one without a match (35%) when it comes to staying at a job. Money is top of mind for many who have big plans for the future, like putting their kids through college (45%), paying off school debt (42%), and buying their dream vehicle (41%). Four in 10 also have dreams to travel, and 33 percent want to retire with comfort.

Survey methodology:

This random double-opt-in survey of 2,000 employed Americans was commissioned by SurePayroll between August 8 and August 9, 2023. It was conducted by market research company OnePoll, whose team members are members of the Market Research Society and have corporate membership to the American Association for Public Opinion Research (AAPOR) and the European Society for Opinion and Marketing Research (ESOMAR).