(© Miljan Živković - stock.adobe.com)

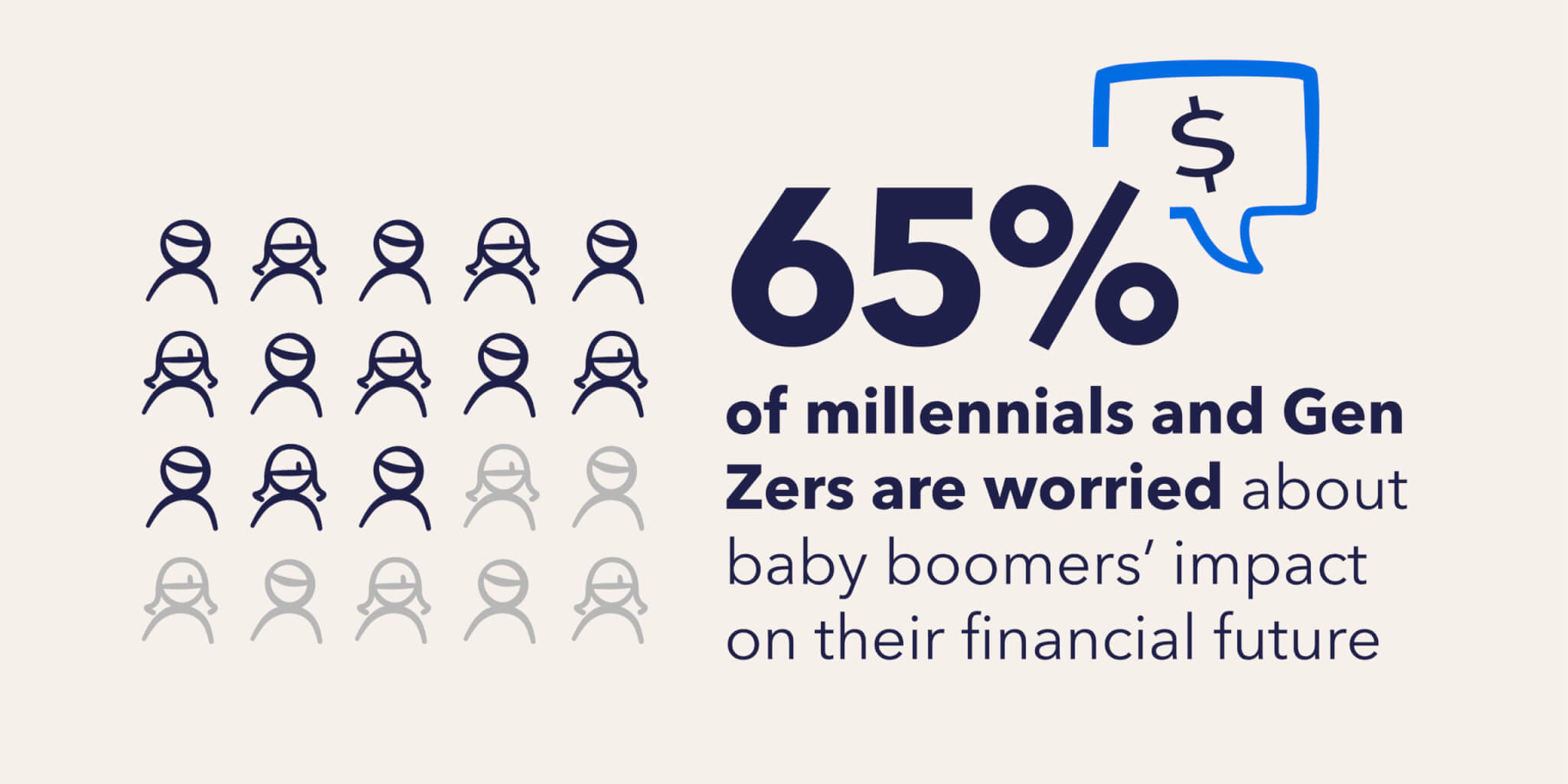

NEW YORK — Sixty-five percent of millennials and Gen Zers are worried about baby boomers’ impact on their financial future, according to new research. A survey of 2,000 U.S. adults evenly split by generation looked at the differences between their financial experiences. Results show that although younger generations are worried about their elders getting in their way, bad money habits are actually common among Americans of all ages.

Just 27 percent rate their money-saving habits as “excellent.” Even though respondents have some good habits, most admit they make poor money decisions sometimes (62%).

The survey, conducted by OnePoll for National Debt Relief, finds that some of the most common bad money habits include writing off small purchases as insignificant (43%), gambling (39%), and using credit cards to pay bills (33%). Respondents say their money habits are inspired by their parents (48%).

Whether these lessons were sound could be up for debate as more than half of Americans have been in debt at some point (51%) and 42 percent are currently experiencing financial difficulties. In light of these financial struggles, many are looking to destigmatize the idea that facing unmanageable debt is “shameful” or embarrassing (36%).

Financial blame game

While millennials were found to take the most responsibility for their habits (71%), a majority of them who are facing financial difficulties still believe their troubles are consequences of baby boomers’ financial decisions (75%). Yet, baby boomers are the most resistant to believing that they make poor money decisions (27%). Of all those who are currently in debt, boomers have the fewest number of respondents who fall into this category (45%).

“This survey confirms something many of us feel, but don’t always talk about: managing money can be tough, and we all make mistakes,” says chief client operations officer at National Debt Relief, Natalia Brown, in a statement. “There’s a lot of guilt and shame people feel when they’re in debt and that needs to change. The data shows that most of us face challenges with money and that none of us are alone in that.”

Millennials also report having the most information about how to create good financial habits (74%) and using it (45%), while boomers say they need more (30%). Gen Z respondents admittedly have the tools and knowledge they need but have not used them (40%).

Nearly a quarter of all respondents feel like they need better knowledge about how to develop good financial habits (23%). This may be why 37 percent look up to industry professionals and 26 percent listen to podcasts or radio shows. Interestingly, influencers have the least financial influence (16%).

Gen Z, particularly, feels like they have a lot to learn from previous generations and would take their elders’ advice seriously (47%). The most important financial lesson that Gen Z and millennials have learned as they’ve aged is how to effectively manage and reduce debt (49% and 61% respectively).

Some advice older generations may be keen to offer the younger crowd is to have an emergency savings fund (61%) and to save and invest earlier (53%).

Although they offer good advice, younger generations expressed concern about paying for others’ mistakes in the future. Between Gen X and baby boomers, the former are nearly three times as likely to recognize that their generation’s financial decisions will have a significant impact on the future of younger generations (23% vs. 9%).

Just 35 percent of older respondents think their generation will leave the economy in a good state for future generations.

“There are many tools and resources available to help people learn and adopt better money habits,” adds Brown. “Regardless of generation, financial literacy and education is important for securing a healthier financial future. By empowering ourselves with smart money habits, we’re not just securing our financial wellbeing, but fostering a culture of fiscal responsibility that will resonate for generations to come.”

Survey methodology:

This random double-opt-in survey of 2,000 general population Americans split evenly by generation was commissioned by National Debt Relief between August 4 and August 8, 2023. It was conducted by market research company OnePoll, whose team members are members of the Market Research Society and have corporate membership to the American Association for Public Opinion Research (AAPOR) and the European Society for Opinion and Marketing Research (ESOMAR).