Photo by Zachary Kadolph on Unsplash

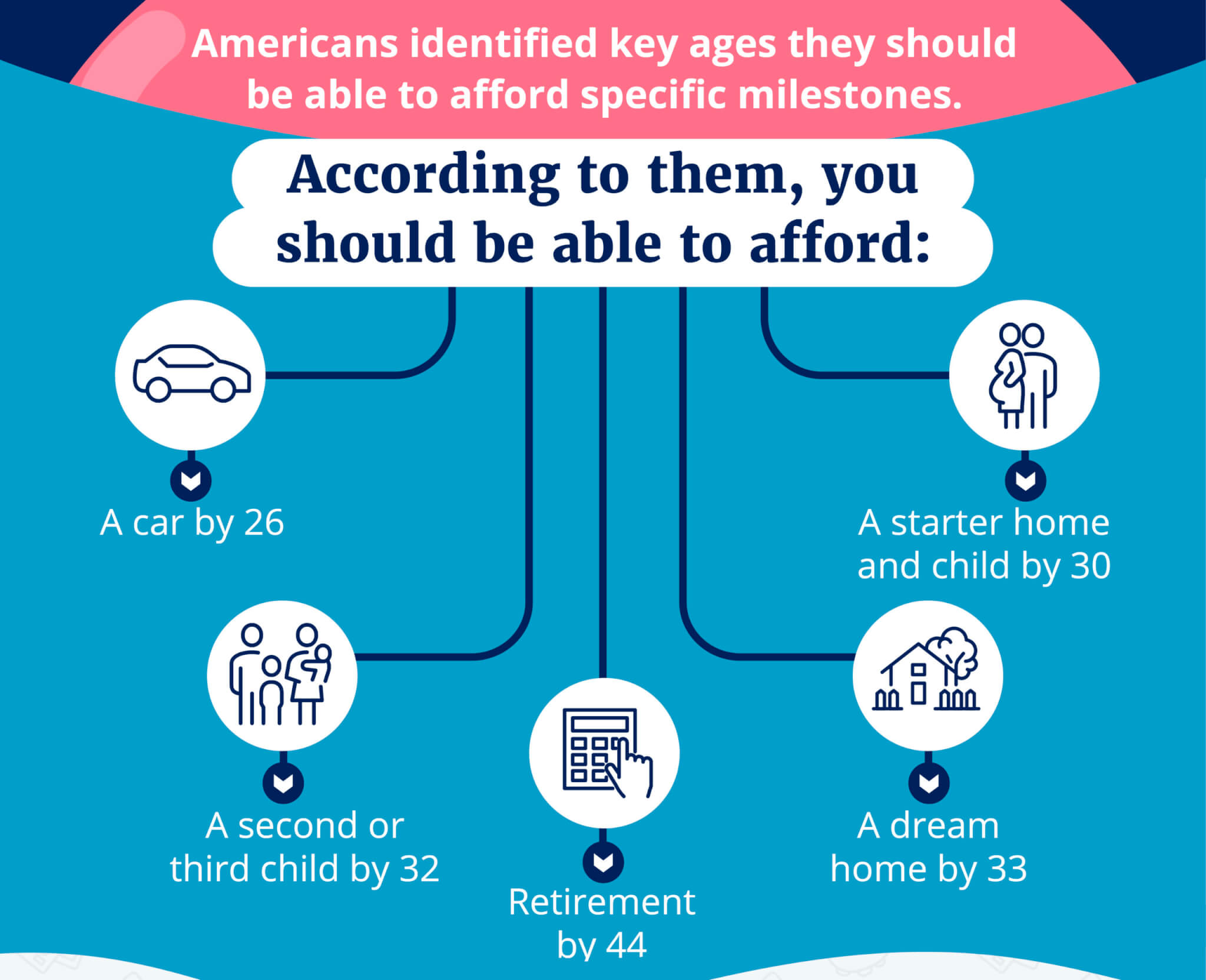

NEW YORK — We’re seeing a lot of research these days emphasizing how more of America’s young adults still rely on their parents financially well into their 20s. Yet according to a new poll of 2,000 adults, Americans believe the average person should be able to afford their “dream home” — by age 33! And if you think that’s wild, the age at which people think retirement becomes attainable is two decades earlier than the standard.

The surprising results reveal that, aside from their ideal house, the average person should also be able to afford a car by age 26, along with a starter home and a child by age 30. After that, Americans should have enough money to have a second or third kid by age 32, and, shockingly, retire by age 44!

Many are making moves toward that goal, as more than half (51%) of those polled say retirement is their top savings goal.

Do you have financial goals?

The study by financial services company Empower, and conducted by OnePoll, finds an overall 56% of people have financial goals— and 92% of those believe their goals are feasible at certain life stages. Additionally, 56% have a budget set aside purely for savings, with individual amounts for both long-term and short-term savings goals.

For short-term goals, defined as attainable within five years of saving, people say they stash an average of $1,539. Savers say they’ve set aside an average of $2,335 for longer-term goals that are five years or more away.

People are more inclined to set aside money for their long-term goals than short-term ones (41%, compared to 24%) which include saving for a home (50%), student loans (46%), medical expenses (45%), and cars (41%).

Long-term savings are also more impactful on peoples’ financial health than short-term savings (78%, compared to 65%).

“Most people believe in the positive impact setting aside money for later can have on their lives,” says spokesperson Courtney Burrell, financial professional at Empower, in a statement. “Whether it be for retirement, a home, or Taylor Swift concert tickets, having a plan — and sticking to it – can help you reach your financial goals, both big and small.”

What’s your money persona?

The study also aims to categorize Americans into four major “money personas”: explorers, builders, mentors, and givers.

Explorers (38%) defined themselves as “learning about the world around them,” builders (37%) are focused on “growing their lives,” mentors (16%) like to “share what they have learned” and givers (7%) believe in “revisiting past aspirations.”

Aligned with their preference to “get the most out of life” by enjoying the here and now (50%), explorers favor saving for material things (83%), whereas builders, mentors and givers prefer saving for experiences (80%, 87% and 83%, respectively).

Nearly half of builders (47%) defined it as “planning for a secure, prosperous future.” And 46% of givers simply says it’s defined by “having nice things.”

“Understanding your financial ‘persona’ and what you value in life can help you make more informed money decisions throughout each stage of your life,” says Burrell.

Survey methodology:

This random double-opt-in survey of 2,000 general population Americans was commissioned by Empower between October 27 and October 28, 2023. It was fielded by market research company OnePoll, whose team members are members of the Market Research Society and have corporate membership to the American Association for Public Opinion Research (AAPOR) and the European Society for Opinion and Marketing Research (ESOMAR).

I guess a great number of people are smoking Crack these days.

Many Boomers are struggling and they have had it pretty easy.

Pipe dream for the lazy and entitled. I’m guessing the people polled are of the generartion that want all the of the pay but without all the work.

The great thing is, nobody is stopping anyone from achieving this.

People need to save more money.

Everyone born before 1975 has had it pretty damn easy, comparitively to most humans in existence.

Everyone born after 1980 has had a very very hard time. Zoomers, born after 1996 will probably have it easier than Millennials, such as myself. After we begin every single life stage, the economy falls out from under us Millennials. No chance!

Were these survey takers in 1st grade? Based on the numbers above – Good Luck retiring at 44 with 3 kids under the age of 14! Also who in the world wants to wait until 26 to buy a car.

What an absolutely COMICAL article. Whoever was polled for these results is not well connected to today’s reality.My 26 YO daughter is a traveling NURSE, brings in very good money weekly BUT it is not steady. Her cost of living expenses are huge…..$3,600.00/month rent alone in Denver, CO for a nice place…..try finding anything decent for less (Good Luck). Her apartment was listed for $4,000.00/month but she got in on a lease back miracle…..but eventually that will expire and it’ll jump up to $4K/month. Even split between 2 people, that’s a big nut to crack…along with car payments, car insurance, Private health insurance, gas, food, utilities.

“SAVING” anything is difficult at best…..the price of everything is sky high,

Just a dumb article not well researched or reality based IMHO!

This just proves reading articles on sf is fake information and time you will never get back

Children should not be a financial decision.

Otherwise, yes staying on a budget and not keeping up with instantgram can make anyone wealthy.

Yes I have been brainwashed by Dave Ramsey.

This article was written to make the working class keep working hard. The elite NEED the working class to keep working hard so they can continue to fund their own lavish wishes. Therefore, they publish articles like this to make you think there is hope. Hope is nothing other than a carrot on a stick. Unless you make $300,000 per year, this is NOT possible. Eventually, the actual average retirement age of 67 will surpass the average life expectancy of 78. At that point, reality is going to get really ugly, really fast.

This is comedy at the highest level, particularly when you are working for someone else at a fixed rate and expect all these things to “magically” happen.

The other thing is that *a lot* of young(er) people are deferring marriage and starting a family for one reason or another; instead, they are living with their parents longer.

Maybe so, because essentially the system no longer wants you by the time you reach you mid-40s. In some businesses, you are out in your late 30s. The longer I go on, the more I think life is like baseball. By your late 30s, if not sooner, you are out of the game. If you don’t make the league soon enough, you will never make the league. Unless you can establish a sinecure for yourself or you have some abundance of prestige and name recognition, once your youth is over and you no longer can live off of your speed, reflexes and youthful stamina, you have no value.

In an economic sense, the view expo9sed here is absurd, at least for most people. As a matter of social apperception, it is spot on. People are expressing their awareness of something they cannot quite name and define in terms of something they can name and define. In art and literature, we call this kind of thing expressionism.

Worked my butt off, sometimes at 3 jobs same day. Worked 31 years for a major auto manufacturer (ass busting work) bought a home at 35, financed for 15 years, invested when I could and retired at 52 y.o. Have great pension and all paid health insurance and now at 80 I have been drawing social security for 18 years also. Retirement at 52 was best thing I ever did.

ok boomer… that was 50s-80s maybe… today is different! Even 100k is not much today

oh yeah $2,335 is what you can barely get after taxes for some…

I’m a boomer and I agree with you. Those were very different times. I grew up in family where only my dad worked at a very low-level government job; my mom stayed home. My parents could not help with college expenses, but I received scholarships, work-study, and grants that enabled me to get a master’s degree by the age of 24, with relatively little student debt. I paid off the loans in two years. My ex-husband and I did buy a house by the age of 26. That’s only because the first two years we worked out of college, we were head residents of a dorm, and had no rent or utilities. We saved as much as we could, and then bought a house. Today that sort of thing could happen for only a handful of people. I think some people of my generation don’t remember how things were back then.

yes, those were the olden days…my dad retired at 50 from Pacbell…he just died at 90. in those days you got pensions and retirements pkgs…he bought our house for 38,000. now zillow says it would go for 1.5 million…yeah, trying buying that working for the telephone company now.

Unfortunately that type of life path is very difficult to follow these days. Pensions are becoming a thing of the past. I’ve been working since I was 15yo; through high school and college. Got a corporate job after college graduation and have now been with that same corporation for over 25 straight years. No pension plan. My ability to retire will depend on the value of my 401K [which I have been contributing to now for over 20 years], savings, and Social Security [if it still exists in 15 years]. Health insurance will be Medicare when I retire [again, if it is still around.] I’m not a frivolous spender. I buy only what I need when I absolutely need it.

I have a friend retiring in a few months in their mid 60’s that made a very good living in sales over the past 40 years. They own their home, no debt, etc. No pension plan. Will be relying on Social Security, Medicare, savings, and 401K for their income.

The results of this survey just make no sense and do not reflect the reality being faced by most Americans today.

More lies…

Agree. This article must be referring to people who get lots of help from their parents, have no student debt, and find a 6-figure job right after they graduate college.

If you are 80, that means you bought your house 55 years ago at 1968 prices.

Based on numbers from amortization.com, allow me to introduce you to some modern realities.

Let’s say you found an impossible starter house today for $200K.

$200,000 in 2023 = $22,843.89 in 1968

$200,000 in 1968 = $1,751,014.74 in 2023

Let’s also look at home prices back then compared to now:

Average home prices for 1968: $24,700

Average home prices for 2022: $454,900

This is reality. Your generation had it easy.

I’m of that generation, and you are correct. I own a home, and I couldn’t even afford to buy it now, and I make a 6-figure annual income with my pension (which most young people won’t have), Social Security, and investment income. This article is crazy.

Most Americans don’t have fat union pensions. So basically, you’ve been living off the work of others for 28 years.

Jeff – the BEST thing(s) you ever did was the planning and heavy lifting early on in your career. I’m afraid the numbers cited in this article suggest way too many are under the impression they can skip that “nuisance” and get straight to the beach – well done, enjoy.

Times have changed considerably since you were in the work force.

The Capitalists have learned how to increase their profits by dramatically lowering wages to the point in some instances where workers need government assistance to survive.

The issue is wealth distribution and right sharing of world resources– not a fundamental change in people’s approach to work, as those who drink the Kool-aid seem to think. The massive frustration we see around us comes from having invested so much of ourselves in a system that is failing so spectacularly. We live in a new gilded age– and that matters to the prosperity (and survival) of the statistical majority in a way that no amount of individual striving can change.

This is the same generation that complains they can’t afford basic rent. How are they going to retire at 44?

Absolute horse sh*t. Pure propaganda.

Which part?

AGREED!!!!

I use to sub. teach math and science and these are the same ones who could not pass 8th grade algebra. They are out of their collective minds, just wait until realility hits. And that would be progressive tax inflation.

The article doesn’t say how the survey participants came up with their info, but it shouldn’t be too hard to create a basic financial simulator for middle/high school kids. Math class seems as good a place as any to introduce it, since you could tie it into the curriculum pretty easily. The goal isn’t to plan out your entire life, but rather to bring assumptions into the open and help manage expectations while there’s still plenty of time to make changes. Might help the kids appreciate parents’ decisions a little, too.

Buffet the Oracle of Omaha sold billions worth of stock YTD 2023 because of the cash supply contraction. (look at historical numbers). I regard his evaluation and predictions of the economy more than 2000 random people during an election cycle packaged by the media hell bent on controlling the narrative to prevent the Orange guy from re-entering the fray.

But obviously didn’t learn how to write a coherent sentence.

The world isn’t collapsing. America is.